Why are so many global equity managers underperforming? Three key questions for investors with underperforming global equity portfolios

Over half of all global equity managers underperformed the benchmark index in 2023, and more than two-thirds have underperformed in 2024—the highest percentage in over two decades.

In Part I of this two-part series, we shared insights on some of the factors driving this phenomenon. In this follow up article, we’ll review key questions that investors should ask if they have an underperforming global equity manager in their portfolio.

Three key questions

Our analysis suggests there are underlying systemic factors which have contributed to recent global equity manager underperformance. In particular, many active managers who have underweighted certain mega-cap US technology companies have trailed the benchmark as enthusiasm for artificial intelligence lifted these stocks higher.

However, not all underperformance has been driven by this market dynamic. Further diligence is required to ensure market-wide factors aren’t masking manager-specific concerns.

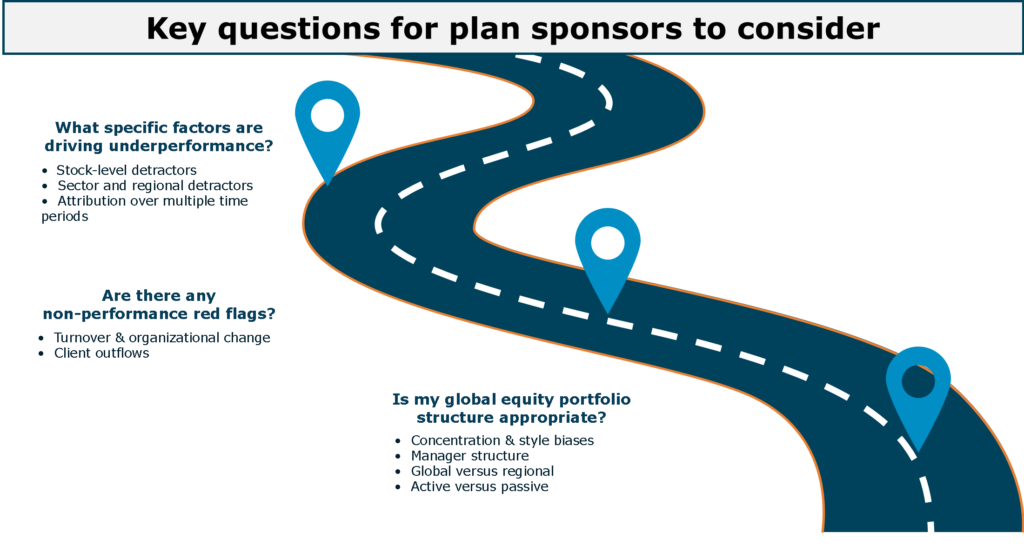

There are two overarching questions that we encourage investors to ask of their underperforming global equity managers:

- What specific factors are driving underperformance?

- Are there any non-performance red flags?

Equally important, however, is the third question for the investor to consider:

- Is my global equity portfolio structure appropriate?

The balance of this installment explores how investors can answer these three key questions.

What specific factors are driving underperformance?

Global equity manager performance may be driven by factors other than the mega-cap US technology company dynamic. Strategy-specific performance attribution will outline the specific decisions which have driven underperformance. A review of performance attribution should include:

- Stock-level detractors. How much of the strategy’s underperformance was driven by lower-than-benchmark allocations to the Magnificent 7? Outside of this group of stocks, which position(s) detracted the most value? Investors may find that underperformance has been driven by stocks unrelated to the themes discussed in Part I.

- Sector & regional detractors. Does the manager exhibit any regional or sector biases that have contributed to underperformance? An underweight to the US or underweight to the Information Technology sector would be consistent with systemic market factors driving recent underperformance.

- Attribution over multiple time periods. Is medium-term underperformance driven by a single bad year of performance, or has the manager consistently underperformed for several years? Strategies that have lagged the benchmark in 2024 & 2023 due to underweighting overvalued companies should have outperformed the benchmark in 2022’s equity market drawdown.

Investors may also wish to revisit their manager’s stated investment philosophy and expected performance in various types of market. For example, some managers will have a stated benchmark-agnostic approach, which seeks a stable absolute return rather than evaluating performance relative to a market-cap weighted benchmark index. Investors should be comfortable with a manager’s objectives, and aligned with their managers on how performance is assessed.

Are there any non-performance red flags?

In determining whether to retain a specific manager, benchmark-relative performance alone may not be a sufficient consideration. Other qualitative considerations include:

- Turnover & organizational change. Have there been any significant personnel changes or organizational disruptions that coincide with the strategy’s underperformance? If so, this could indicate that underperformance is driven by an issue specific to the strategy that is expected to persist, rather than a transitory market condition.

- Client outflows. Has the strategy lost significant client assets due to their underperformance? If so, does the magnitude of outflows introduce concerns about the firm or strategy’s future viability?

Is my global equity portfolio structure appropriate?

In addition to manager-specific factors, investors may wish to take a more holistic view of how their exposure to global equities is structured. Key aspects of global equity portfolio structure include:

- Concentration & style biases. Strategies with strong style biases or concentrated portfolios will tend to exhibit higher tracking error relative to the benchmark. Monitoring these specialized mandates may require additional education and expertise, and often requires that investors be comfortable with prolonged periods of benchmark-relative out- or under-performance.

- Manager structure. Does the current number of managers and strategies in your global equity portfolio align with your governance capacity, while controlling manager concentration risk? The optimal number of managers in an equity portfolio may evolve over time as fund assets increase or decrease. In combining two or more equity managers, investors should also consider how the strategies will complement each other in a total portfolio context.

- Global versus regional. Global mandates provide flexibility for an active manager to allocate to the best investment opportunities available, regardless of location. If implemented successfully, this regional allocation decision can provide an additional source of alpha. However, a regional specialist manager may be more skilled than a global manager in selecting stocks for their particular region.

- Active versus passive. Active managers aim to provide higher returns and/or lower volatility than the benchmark index, but will generally charge a higher management fee than an index fund. The governance time and effort required to select and monitor an active manager may be another consideration in deciding between an active versus passive approach.

Additional considerations for Capital Accumulation Plan sponsors

In a Capital Accumulation Plan, plan sponsors design an investment menu for plan members to choose from, but plan members ultimately make the investment decision. Plan sponsors may offer more than one option for global equity investment, in order to suit differing member preferences.

Therefore, in addition to considering a global equity manager replacement, Capital Accumulation Plan sponsors may wish to revisit the number and type of global equity investment options made available to members. Potential investment menu changes include:

- Offering more than one global equity option, particularly when one strategy exhibits a strong style bias or high tracking error relative to the benchmark;

- Offering passive investment options alongside active options; and

- Allowing members to allocate regionally to separate US, EAFE (International) and Emerging Market strategies.

Signs of shifting markets in 2025

Finally, investors may take heart that equity market tides appear to be turning in 2025. Over the first two months of the year, the CNBC Magnificent 7 Index fell 6%, while the Bloomberg US Large Cap ex Magnificent 7 Index was up nearly 5%.

This reversal has brought some relief to active managers. Sixty-two percent of global equity managers have outperformed the MSCI ACWI Index over the first two months of the year – nearly double the 32% of managers who outperformed the index in 2024.